Condo prices in Toronto carve out two-year low, house prices just a hair behind.

By Wolf Richter for WOLF STREET.

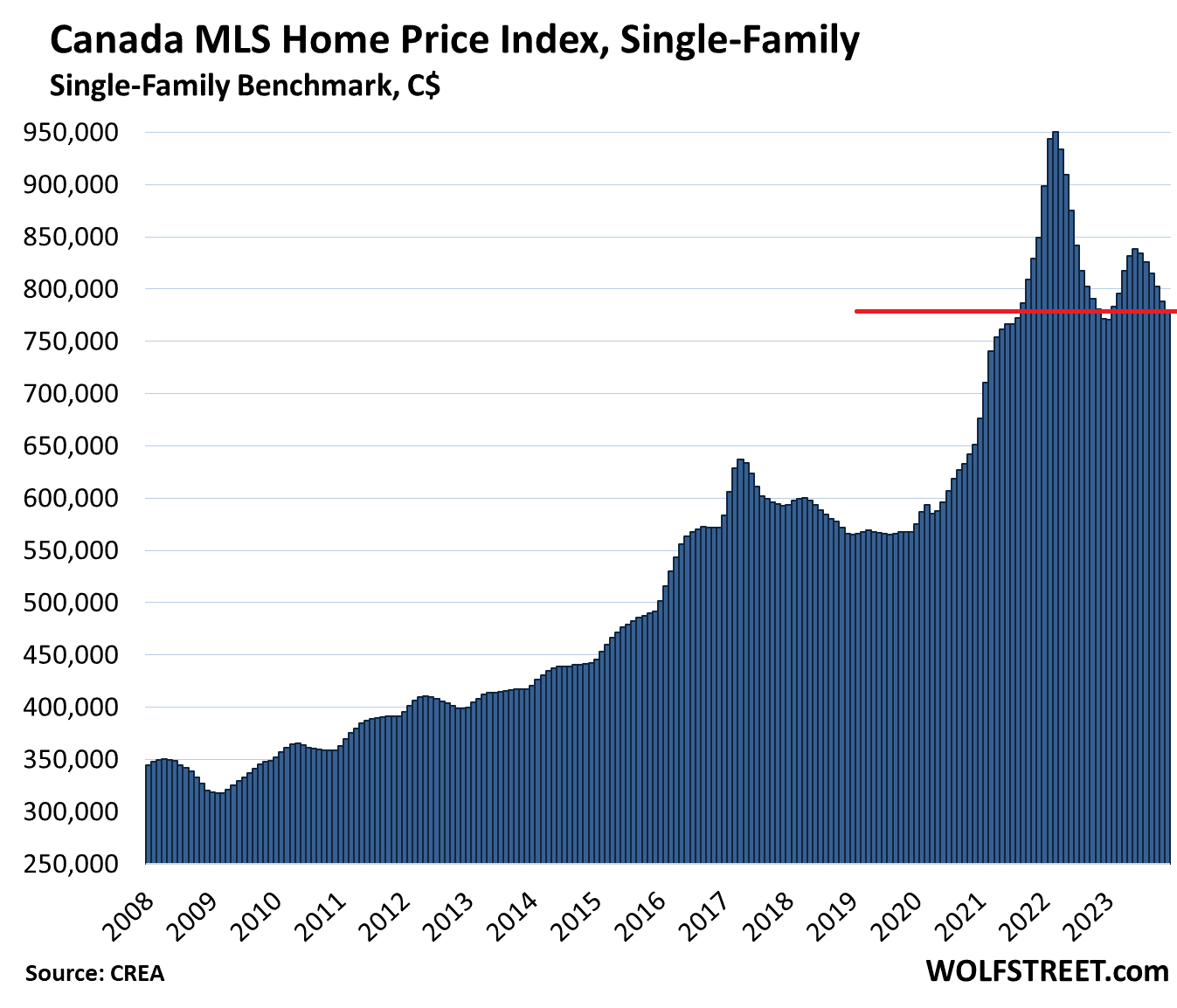

House prices in Canada have now fallen by 18% from the peak in March 2022 – or by $171,500 (all in Canadian dollars) – after the 1.2% drop in December from November, the sixth month-to-month drop in a row, according to the Home Price Benchmark Index for single family houses by the Canadian Real Estate Association (CREA) today.

This brought the national price down to $779,100, the level first reached on the way up in September 2021. Compared to December a year ago, after the massive drops in 2022, the price was up by 1%.

Big losses spread across most of the major markets. And even in Calgary, prices dropped from the record. We’ll get to the individual markets in a moment.

Home sales in December rose by 3.7% from a year ago; and on a seasonally adjusted basis by 8.7% from November. But for all of 2023, home sales fell by 11% from 2022, making it “the lowest annual level for national sales activity since 2008,” CREA said.

“Was the December bounce in home sales the start of the expected recovery in Canadian housing markets? Probably not just yet,” said Shaun Cathcart, CREA’s Senior Economist. “It was more likely just some of the sellers and buyers that were holding onto unrealistic pricing expectations last fall finally coming together to get deals done before the end of the year.”

The problem is that prices are too damn high, inflated by years of the Bank of Canada’s near-0% interest rate policy and by its massive QE during the pandemic.

The end of easy money.

The Bank of Canada has tightened policy, the easy money is over, it hiked its overnight rate to 5.0% in July and has kept it there. Inflation in goods and energy has vanished, prices have come down, but in services, inflation is hot and isn’t backing off, and inflation in rents has exploded. The Bank of Canada doesn’t appear to be eager to fuel this inflation with rate cuts, and it has taken a careful wait-and-see approach.

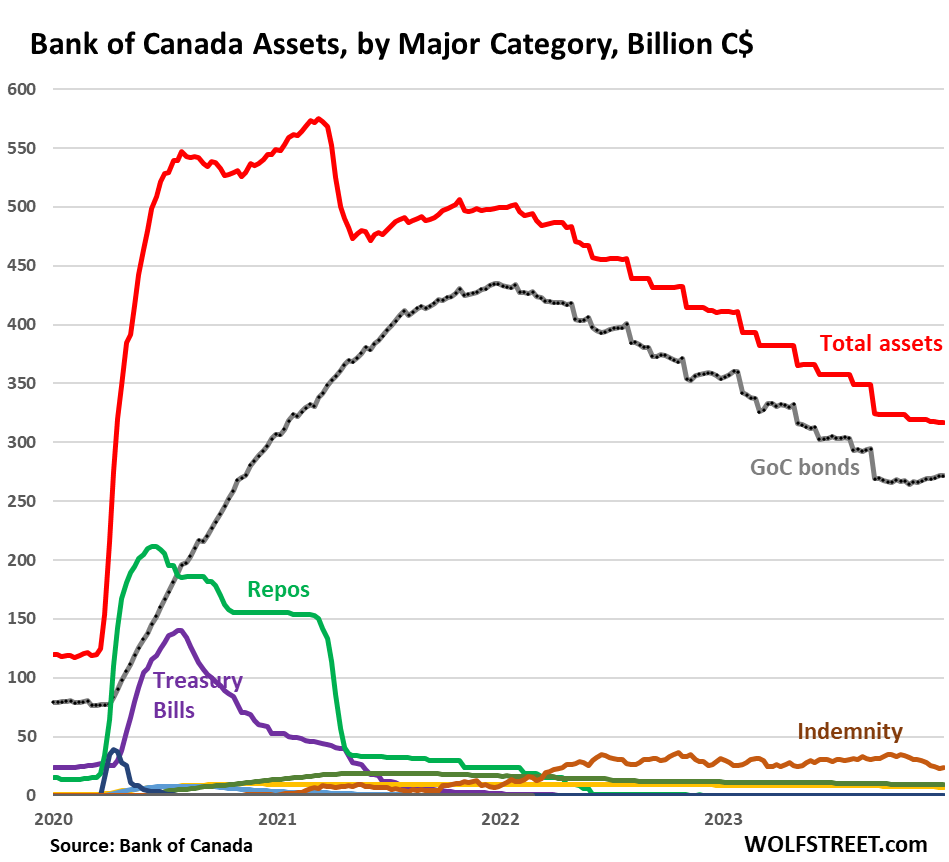

At the same time, the Bank of Canada is unwinding the results of its massive money-printing during the pandemic and has already shed 57% of the $455 billion in QE assets that it had added during the pandemic.

There is still aways to go to drain the crazy liquidity thrown at the markets during the pandemic, and more will drain this year, including on February 1, March 1, and April 1, when some big chunks of the Bank of Canada’s holdings of Government of Canada (GoC) bonds mature: $33 billion combined is scheduled to come off by April 1. In other words, over the next three months, the BoC’s total assets will drop by another 10%:

Single-family House Prices by Market.

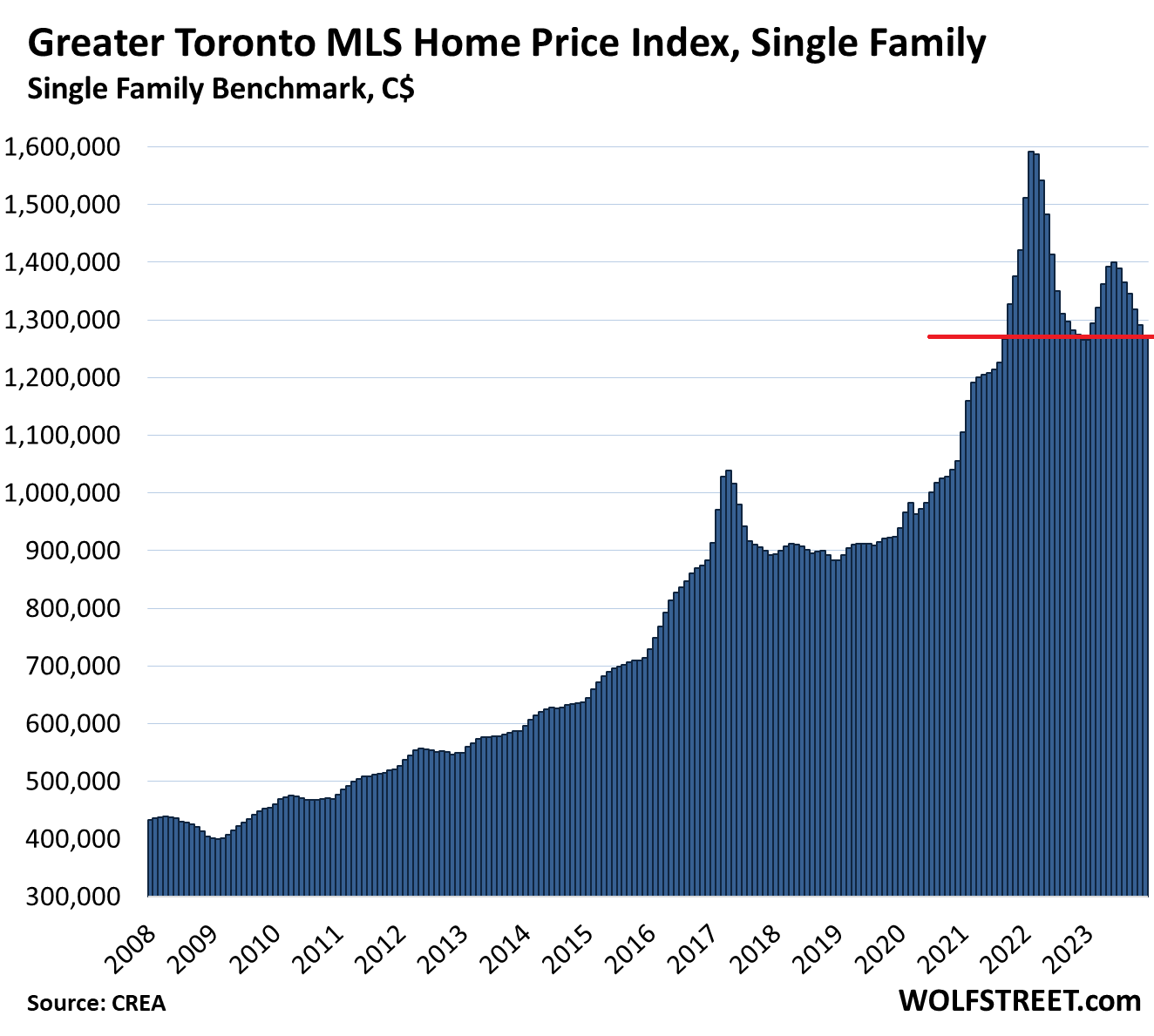

Greater Toronto Area (GTA): The MLS Home Price Benchmark Index for single-family houses fell by 1.4% in December from November, to $1,273,300, the sixth month in a row of declines. The drop whittled down the year-over-year gain to 0.6%.

The benchmark price has plunged by 20.0%, or by $317,700, since the peak in February 2022 and is now below where it had first been in September 2021 on the way up, and is just a hair from carving out a two-year low:

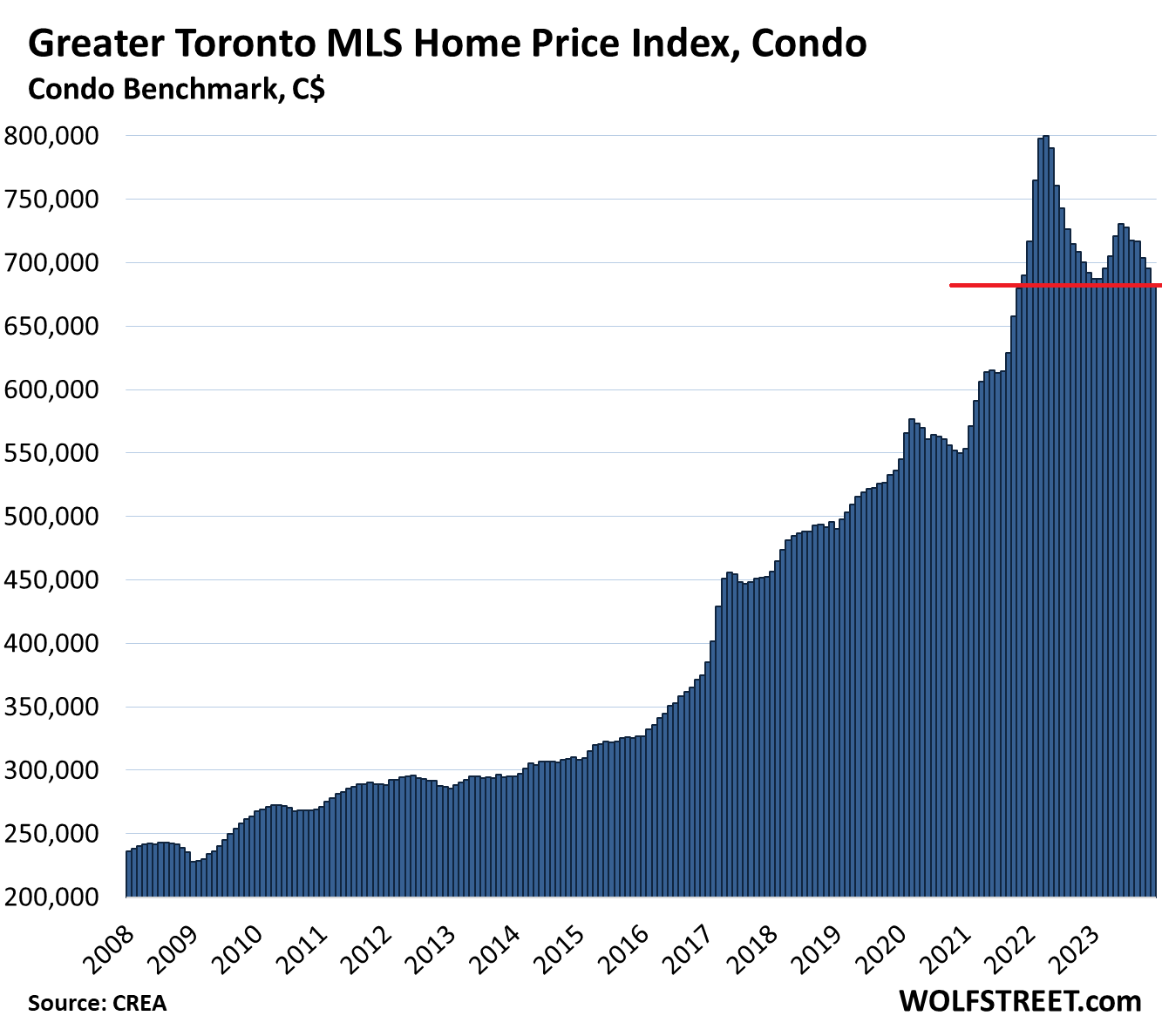

For condos in the GTA, the benchmark price dropped by 1.7% in December from November, by 1.3% year-over-year, and by 14.6% from the peak in April 2022, to $683,200. And it has successfully carved out a two-year low:

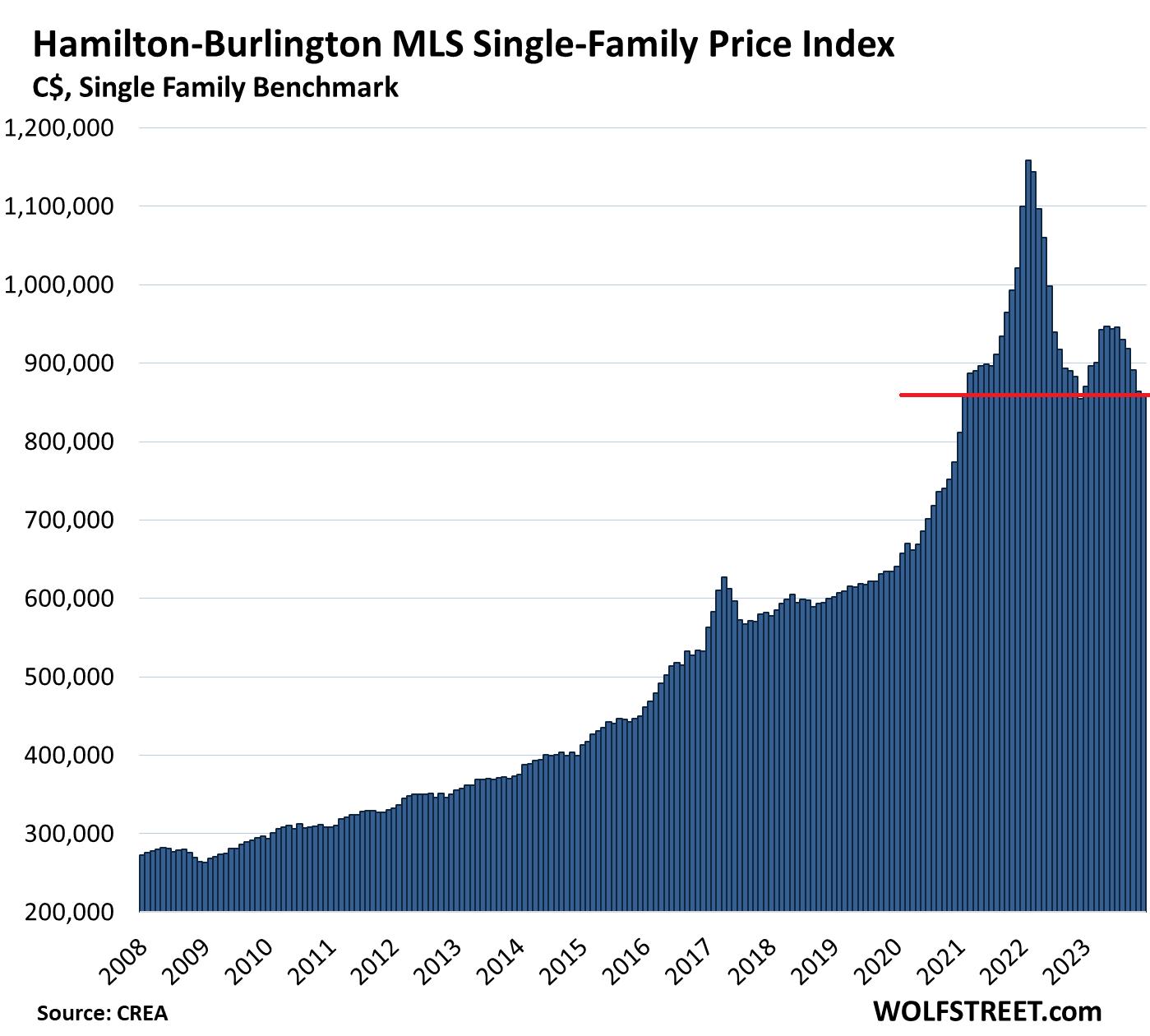

In the Hamilton-Burlington metro (part of the “Greater Toronto and Hamilton Area”), the single-family benchmark price declined by 0.4% in December from November, to $861,100, a hair from carving out a two-year low.

- From peak in February 2022: -25.7%, or -$297,800

- Year-over-year: +0.8%.

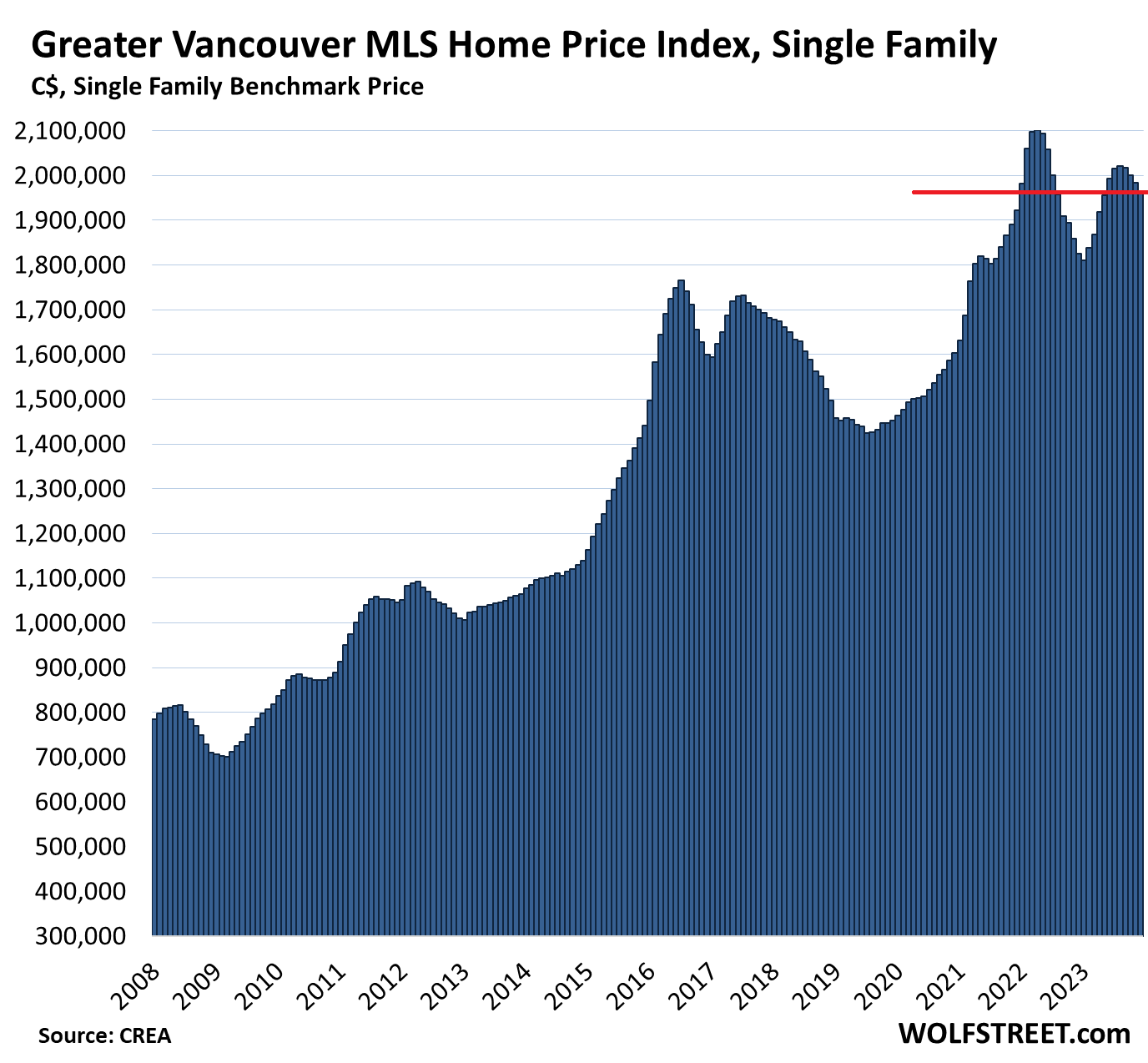

Greater Vancouver: The benchmark price for single-family houses fell 1.0% for the month, to $1,964,400:

- From peak in April 2022: -6.6% or -$137,700

- Year-over-year: +7.6%

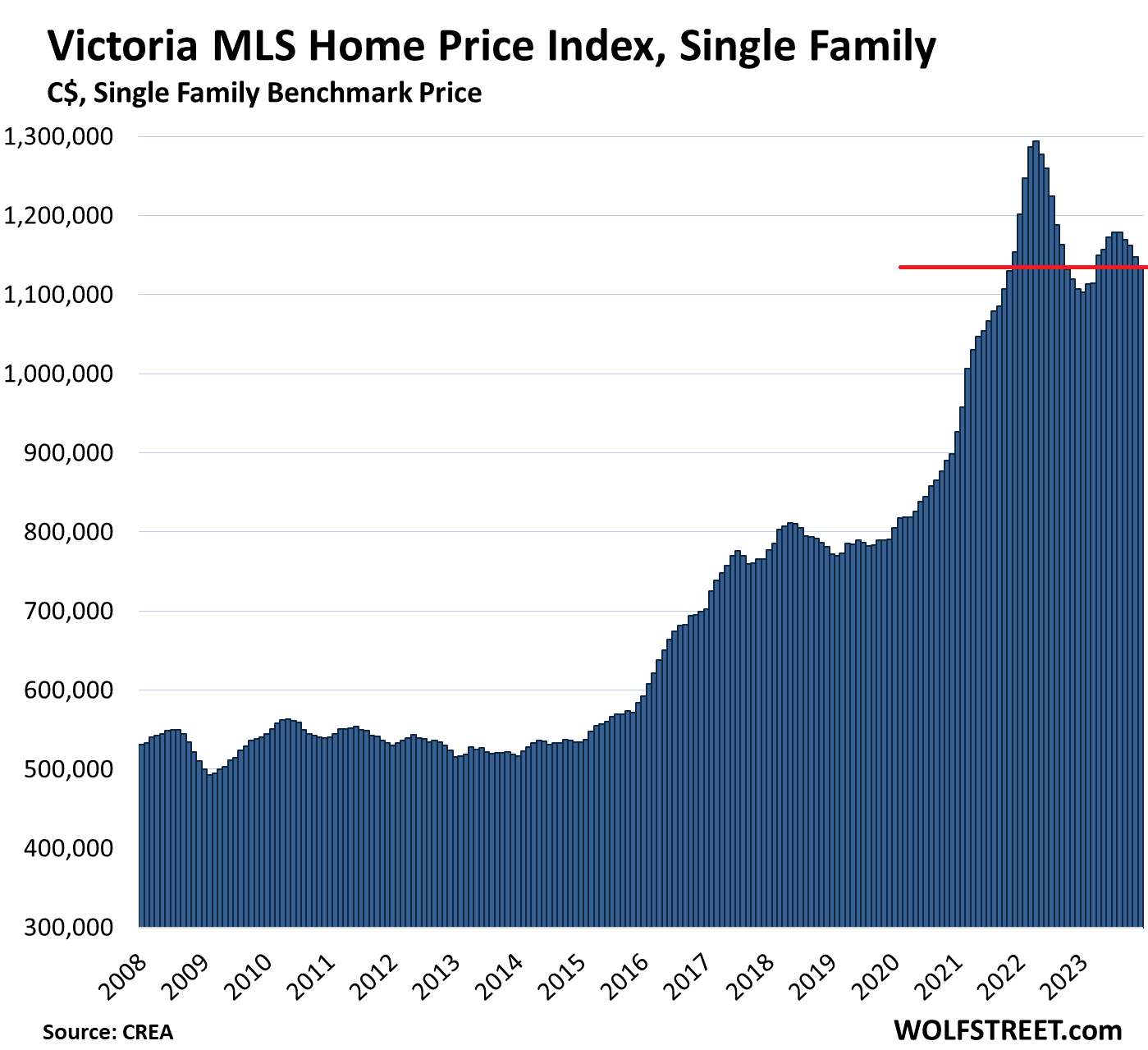

Victoria: The single-family benchmark price fell by 1.2% for the month to $1,134,600 million:

- From peak in April 2022: -12.3% or -$159,800

- Year-over-year: +2.5%

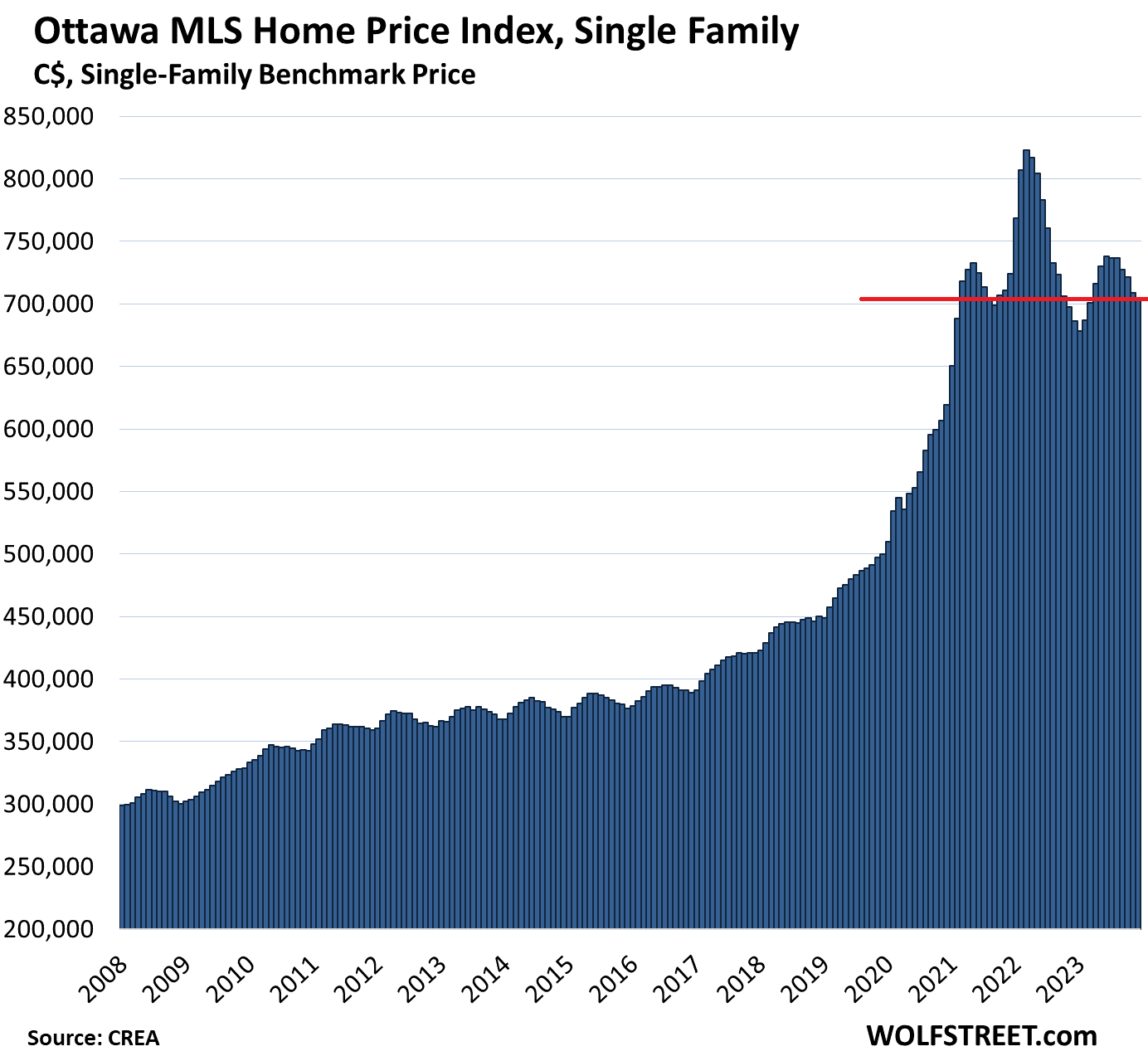

Ottawa: The benchmark price of single-family houses fell by 0.6% for the month, to $704,900, below where they’d first been in March 2021:

- From peak in March 2022: -14.4% or -$118,300

- Year-over-year: +2.7%.

A head-and-shoulders chart for the housing market.

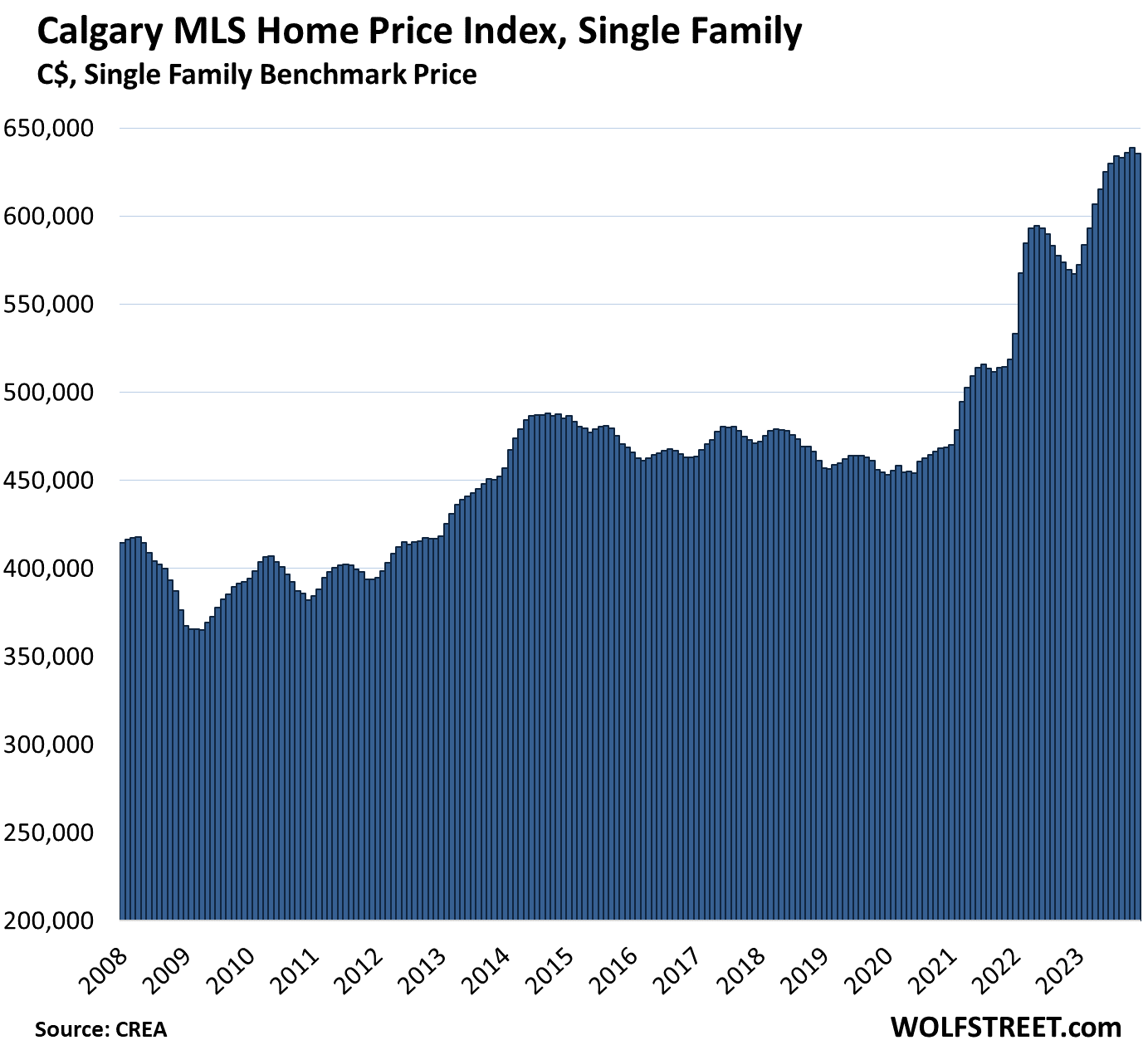

Calgary: The single-family benchmark price fell by 0.5% for the month to $635,600, having now roughly flatlined for the past four months, after the big surge earlier in 2023. Year-over-year, the benchmark price was up 12.1%. Note how prices essentially went nowhere between 2008 and mid-2020, when the effects of money printing and the renewed oil boom kicked in.

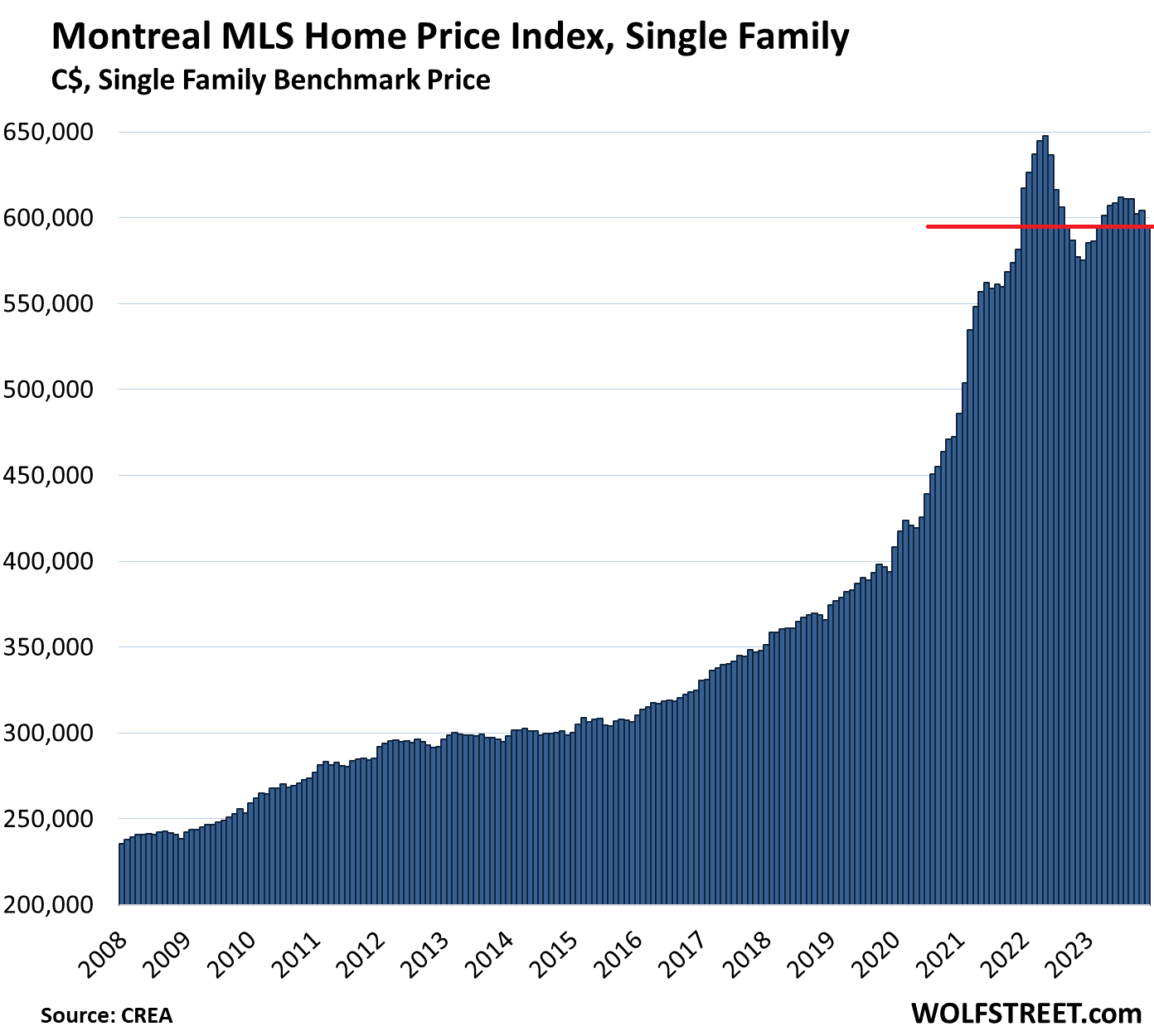

Montreal: The single-family benchmark price fell by 1.4% for the month, to $595,600:

- From peak in May 2022: -8.0% or -$52,000

- Year-over-year: +3.5%

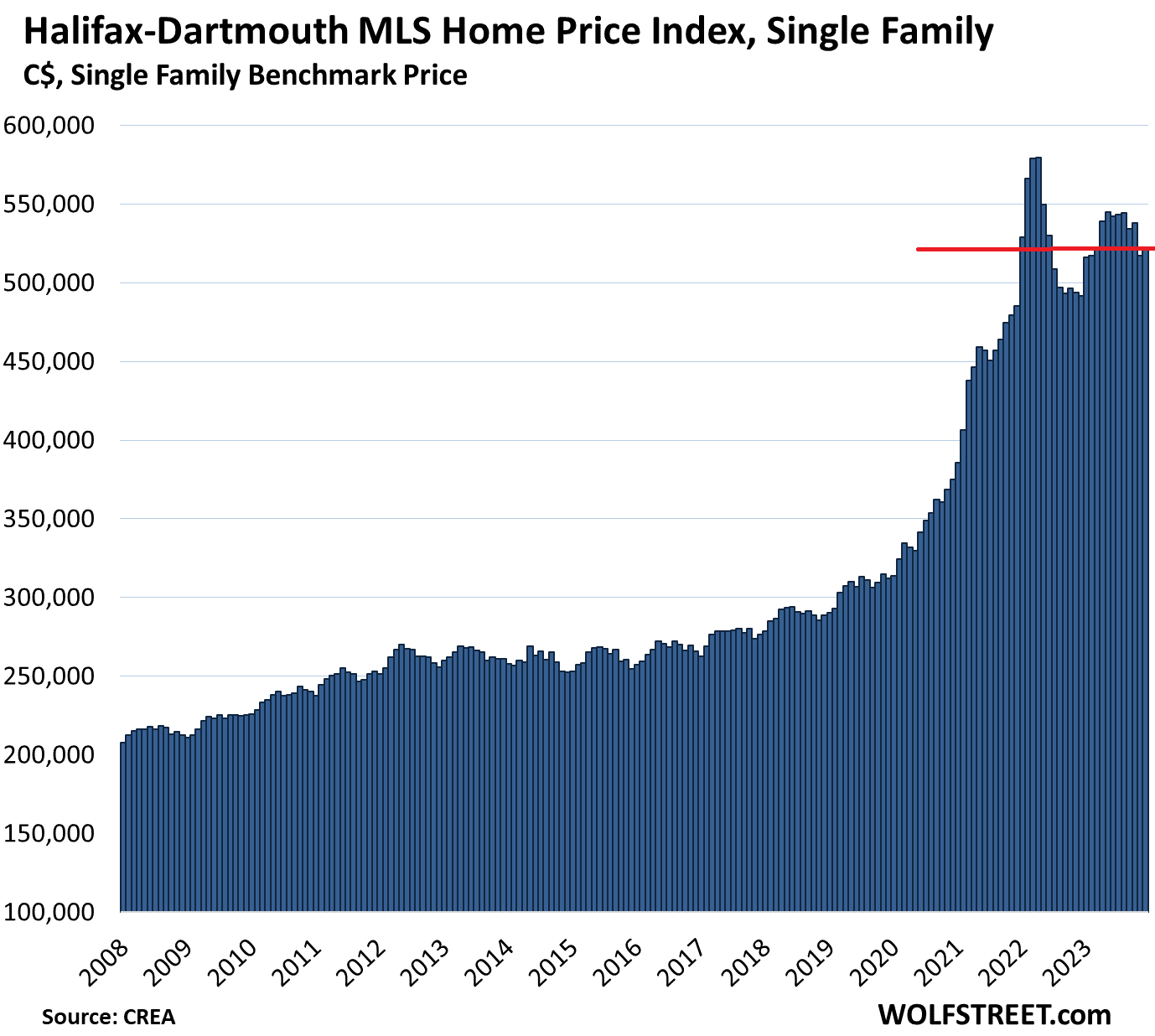

Halifax-Dartmouth: The single-family benchmark price ticked up by 0.7%, after the 3.9% plunge in the prior month, to $520,800:

- From peak in April 2022: -10.1% or -$58,700

- Year-over-year: +5.9%.

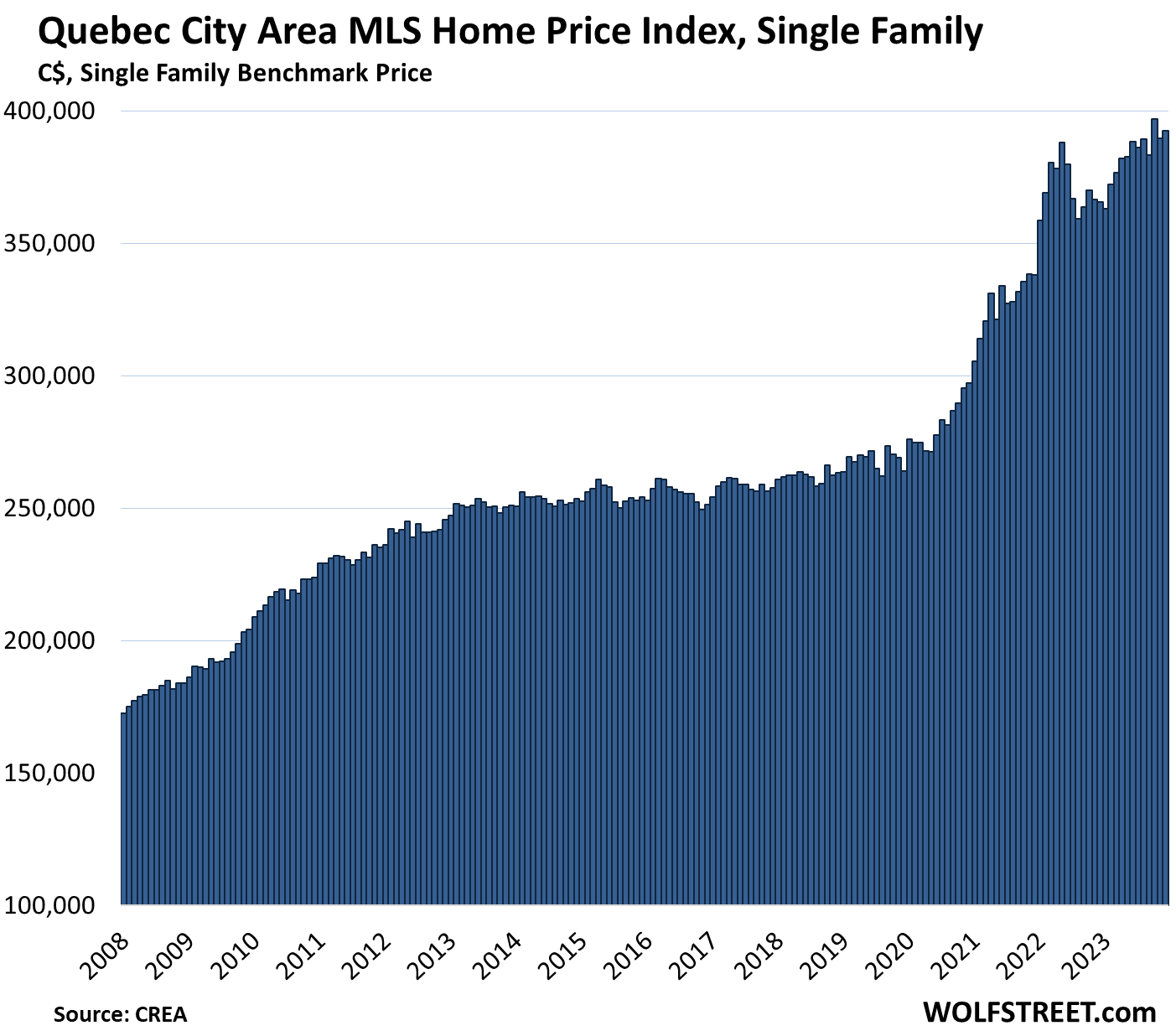

Quebec City Area: The single-family benchmark price rose by 0.7%, to $392,500 and was up by 7.4% year-over-year. October had set a new high: